Treasury Clearing's New Toolkit

How CCPs are reshaping margin andcollateral

What the CME–DTCC cross-marginingexpansion signals about the next phase of U.S. Treasury clearing

AT A GLANCE

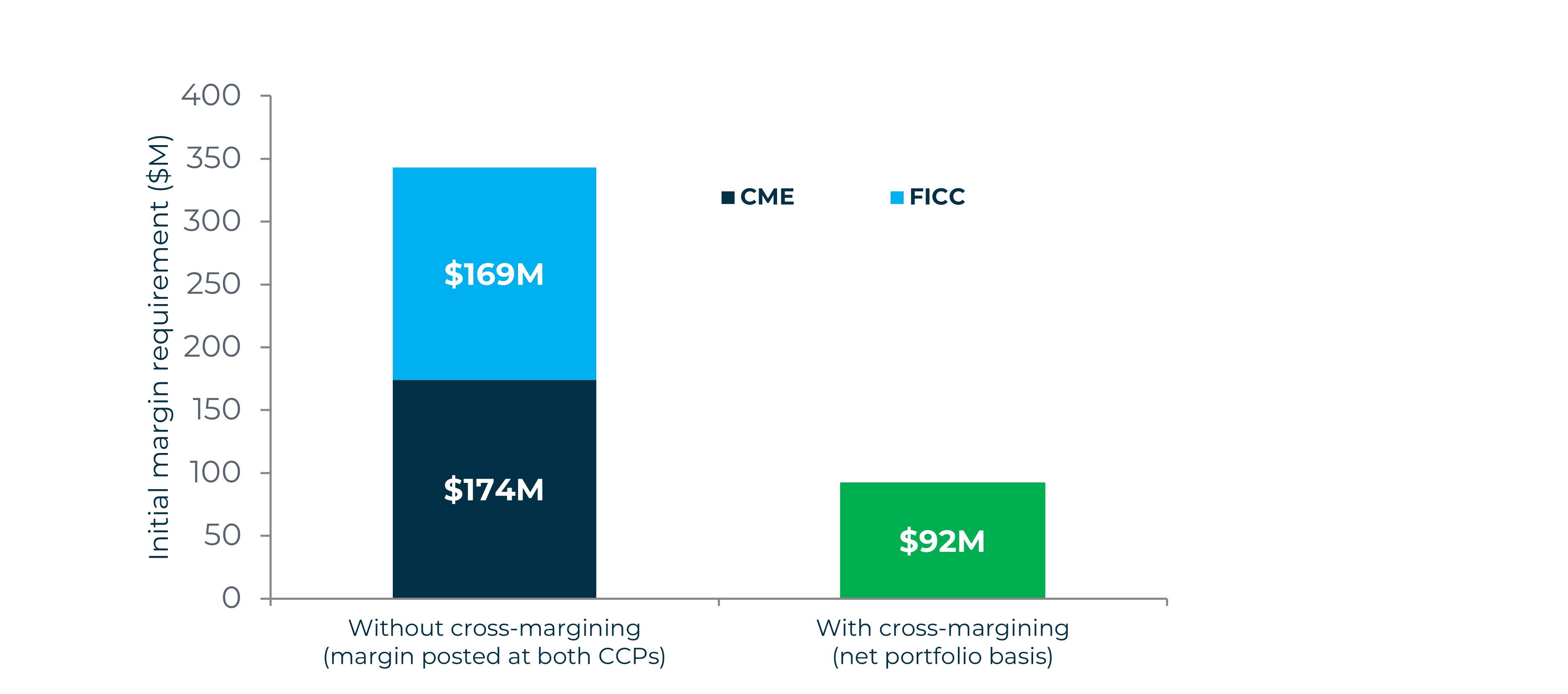

From 30 April 2026, customer-level cross-margining between FICC-cleared U.S. Treasury positions and CME-cleared interest-rate futures is available for eligible accounts. The biggest beneficiary is the cash-futures basis trade. Customers running offsetting cash and futures legs no longer post margin twice; instead the two legs are margined as a single net portfolio.

▸ Marginsavings capped at 80%:

On positions allocated to the newcross-margin (XM) accounts.

▸ Eligibility is limited to specific FCMs:

Only dually-registered BD-FCMs that are common members of CME and FICC qualify. Positions held elsewhere remain margined separately at each CCP.

▸ Bank capital is the unfinished piece:

Until U.S. Basel III aligns with the CCP risk model, dealer balance sheets may not reflect the full netting benefit, capping how much efficiency reaches clients.

A market reaching for safety, without losing liquidity

Cross-margining between FICC-cleared Treasury positions and CME Treasury futures has become a critical tool for managing capital in the evolving U.S. Treasury market - a market whose fragility was made vivid in March 2020 when hedge funds unwinding the cash-futures basis trade overwhelmed dealer balance sheets.

The SEC's 2023 clearing mandate, which requires clearing of cash trades by 31 December 2026 and repo by 30 June 2027, introduces the potential for “double margining” - customers running offsetting positions could otherwise post collateral separately at FICCfor the cash and repo leg and at CME for the futures leg. This can significantly raise working capital requirements and constrain participation by leveraged market intermediaries, who play a central role in market liquidity. Cross-margining allows economically offsetting positions across cash, repo and futures to be recognised as a single risk portfolio for margin purposes, materially reducing total margin obligations. The program is designed to keep the intermediaries the market depends on active - preserving the leveraged liquidity provision on which the Treasury market relies.

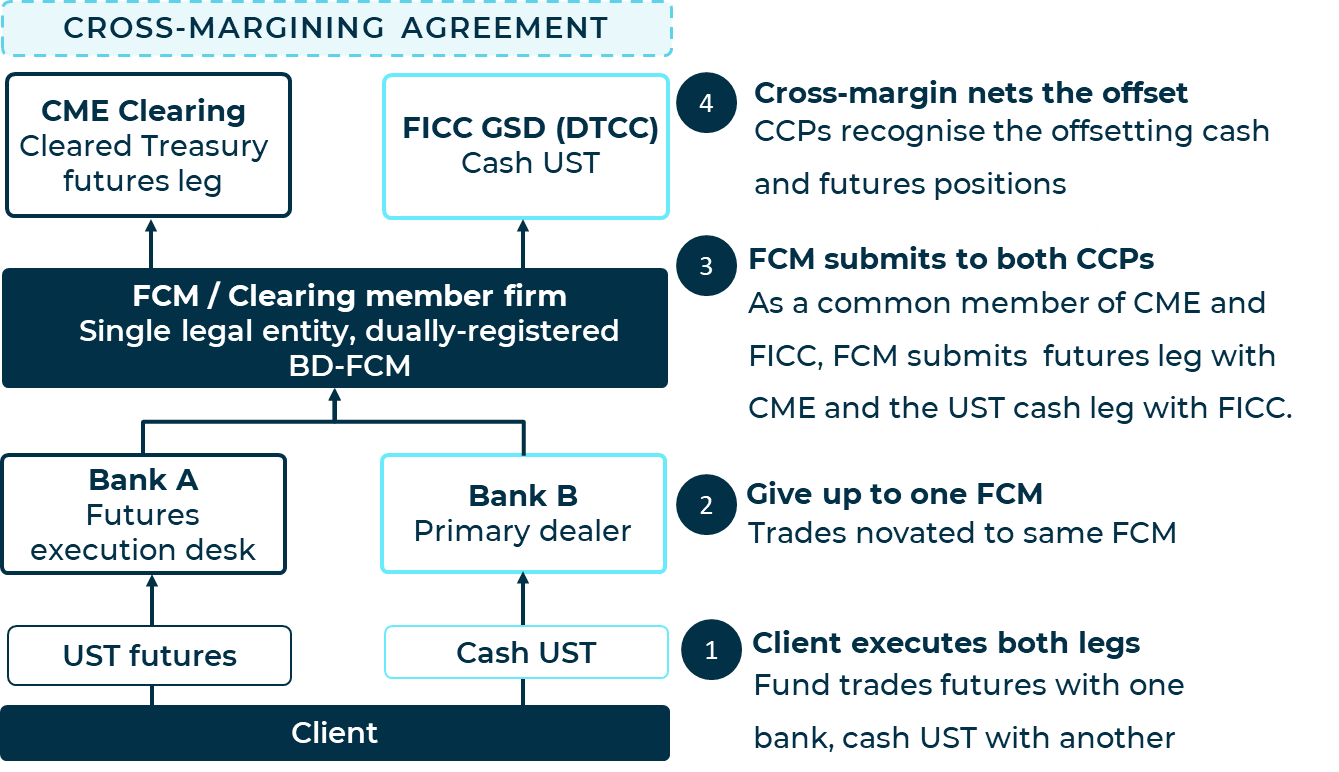

How it works

The program operates within a tightly defined perimeter. Eligible customers must qualify as Sponsored Members or Executing Firm Customers under FICC's rules; eligible products are U.S. Treasury cash and repo with more than one year to maturity. MBS, TIPS, and Treasuries within one year are excluded. Within that perimeter, the architecture is built around a single clearing path: a client's two trades originate at separate execution desks, flow via give-up to a single clearing FCM, and reach the two CCPs, where the Cross-Margining Agreement nets the offsetting risk into a singleinate at separate execution desks, flow via give-up to a single clearing FCM, and reach the two CCPs, where the Cross-Margining Agreement nets the offsetting risk into one margin call.

Figure1. How the program is structured

Within that structure, the program operates on a daily five-step cycle between FICC, CME's hosted optimiser, and the clearing member firm.