In Tonic's first release of detailed UST Clearing content, we will define the scope of the rules, discuss program lifecycle with key decisions, and then share the core FICC GSD membership types and ways to access central clearing.

Scope Summary

The SEC’s US Treasury Clearing rules will drive the most significant period of transformation across the US Treasury market since inception.

The US Treasury market is a bedrock of the global financial system with around $27 trillion outstanding, playing a critical role to facilitate liquidity and resilience across the investment world.

For that reason, the impacts of mandatory UST Clearing run deep for in-scope firms and UST ecosystem players, driven by the market’s high dependence on US debt instruments, specifically cash-settled trades and repo agreements.

But who is in-scope?

For UST Cash Trades - Most market-making firms, or broker/dealers i.e. firms that are counterparty to both buyer and seller in two separate transactions.

For UST Repo Trades - Almost all firms that trade UST Repo. If one counterparty in a UST repo trade is a Direct Participant of FICC GSD, which includes most major dealers, the transaction must be centrally cleared. This key concept pulls the buy-side into the regulation.

Note that FICC GSD is the only CCP available to Centrally Clear USTs today, however, the direct participant inclusion logic would apply to transactions with other CCPs as they enter the UST clearing space.

And when is regulatory compliance due?

Effective dates are staggered across the two UST transaction types. All in-scope trades must be centrally cleared once we hit these dates.

For UST Cash Trades - Compliance date is December 31, 2025.

For UST Repo Trades - Compliance date is June 30, 2026.

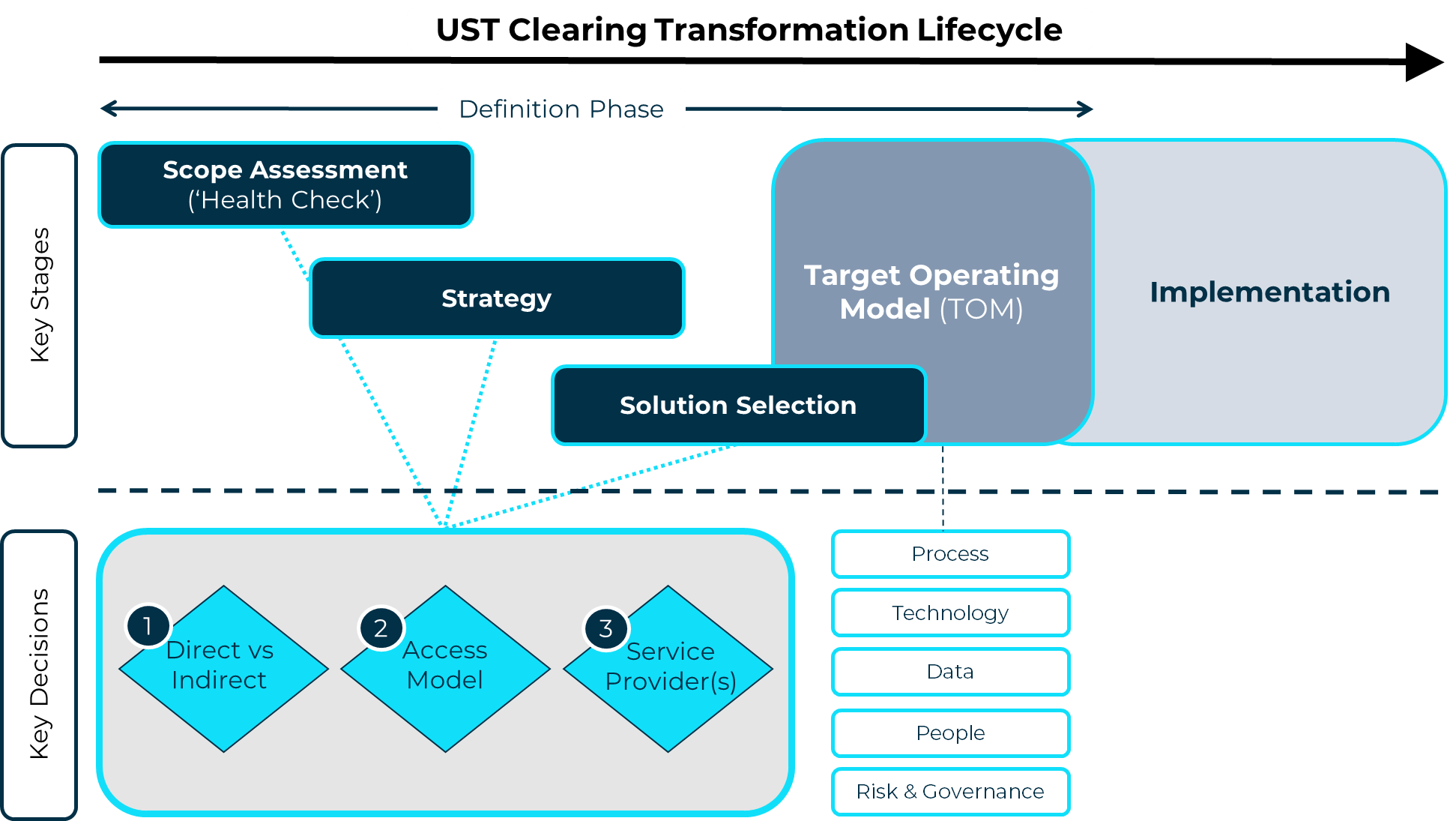

The UST Clearing implementation lifecycle will be long and complex, playing out over the next couple of years.

All firms will have to move through broadly the same set of program phases until go-live. These phases typically include scoping, strategy, solution selection, target operating model definition and then implementation.

The below diagram reflects the core UST Clearing activities that firms will need to follow, including the key early decisions.

At the start of any UST Clearing program, all firms will need to perform a scope impact assessment, or ‘Health Check’, in Tonic speak 😊.

Key outcomes of the Health Check should be a strong understanding of:

The firm’s current state UST clearing footprint (products, volumes, revenue & costs, operating model, etc)

The different UST clearing models available, including the respective financial and operational impacts

This information will provide high-value data for key early decisions that all in-scope firms will need to make to shape their future UST Clearing operating model, including:

Direct vs Indirect access to the Central Counterparty

If firms use an indirect model, further decisions will include:

The preferred Access Model used i.e. Sponsored Services vs Agent Clearing (‘Done-With’ vs ‘Done-Away’ models)

The chosen Service Provider(s) for Central Clearing

Once these decisions have been made, a firm can define the UST Clearing target operating model, or ‘TOM’, and then begin the Implementation phase to ensure go-live readiness.

Given that FICC GSD is currently the only existing CCA, or CCP (Central Counterparty), for US Treasuries, we will focus on FICC’s membership types and access models within this piece.

We acknowledge the recent public announcements from CME and ICE that they will build new CCA (Covered Clearing Agency) services for USTs, with the potential for additional providers to join the mix. However, there is limited information available on these providers today.

Stay tuned for additional Tonic information on additional Central Clearing offerings from other approved CCAs, once the information becomes public.

Direct vs Indirect Access

The initial UST Clearing decision that firms will face is whether they want to set up with direct or indirect access to FICC GSD.

Direct access requires connectivity to FICC GSD for trade novation, matching and settlements, as well as responsibility for clearing fund and margin obligations. As such, direct access to FICC GSD comes with high costs and operational burden. Historically, this has led to only the largest banks and securities dealers adopting this model.

Indirect access, on the other hand, means a firm is reliant upon another firm to clear USTs on their behalf. Indirect access does not require operational connectivity to FICC GSD and has no direct obligation for clearing fund or margin obligations.

The indirect model is a much lighter operational touch and less hassle for many firms. For that reason, indirect membership is typically preferred by the buy-side community.

FICC Membership Types & Access Models

Now we’ll go one level down and zoom in on the different membership types and access models available at FICC GSD, both direct and indirect.

See the summary table below to compare the key traditional FICC GSD memberships and access models.

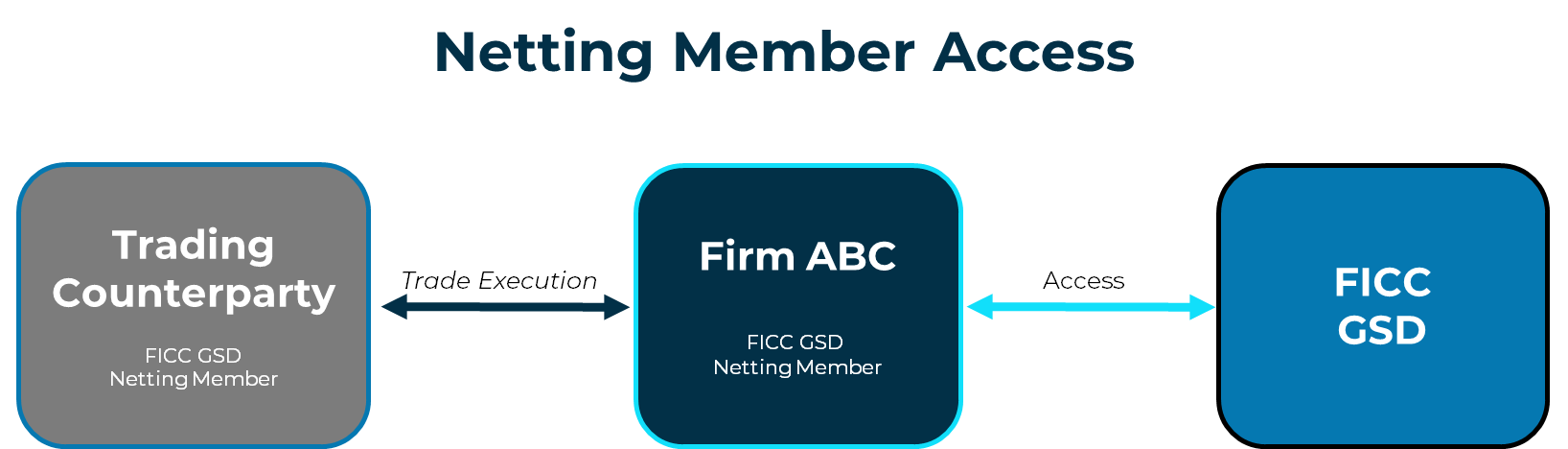

Firstly, it’s important to be aware that those firms who have direct access to FICC GSD are signed up as full ‘Netting Members’.

Historically, under ‘Netting Membership’, there are two core types of activity:

Firms who clear their house trades directly with FICC GSD

Firms who clear trades on behalf of other firms, or ‘Sponsoring Members’

Netting Members are direct participants at FICC GSD, which means they must meet qualifying criteria, operationally connect to FICC GSD and support all clearing fund and margin obligations. They must run all central clearing workflows for their House trades once executed in the market

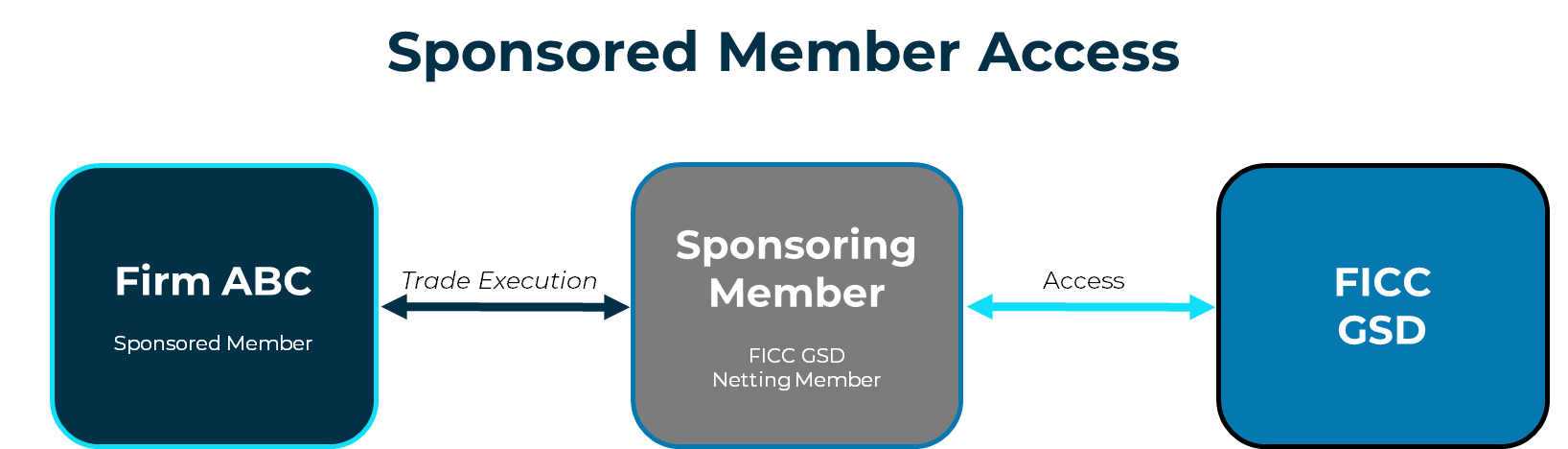

Sponsoring Members are full Netting Members of FICC GSD who also clear trades for clients that they trade with (all trades are 'Done-With' today, but 'Done-Away' can also be supported in the sponsored model). They run the same operational functions and retain full financial obligations across both House and Client trades.

Sponsored Membership is a limited GSD membership for the clients of the Sponsoring Members. Sponsored Members are typically buy-side firms – they do not connect directly with FICC GSD and they rely upon the Sponsoring Members for all operational workflows and clearing fund/margin obligations.

A key point about today’s FICC GSD Sponsored Service is that the Sponsored Member (e.g. buy-side firm) trades directly with the Sponsoring Member, before that trade is cleared with FICC. We are expecting Sponsoring Members to support clearing for 'Done-Away' trades in the near future (no one supports today).

In recent years, buy-side firms have elected to set up withmultiple Sponsoring Members, to give them access to multiple trading partners for centrally cleared repo (we will explore this in our UST Clearing Kickstarter Part 2, section), to reduce concentration risk and give them themselves broader liquidity and price discovery.

The 'New' Agent Clearing Model

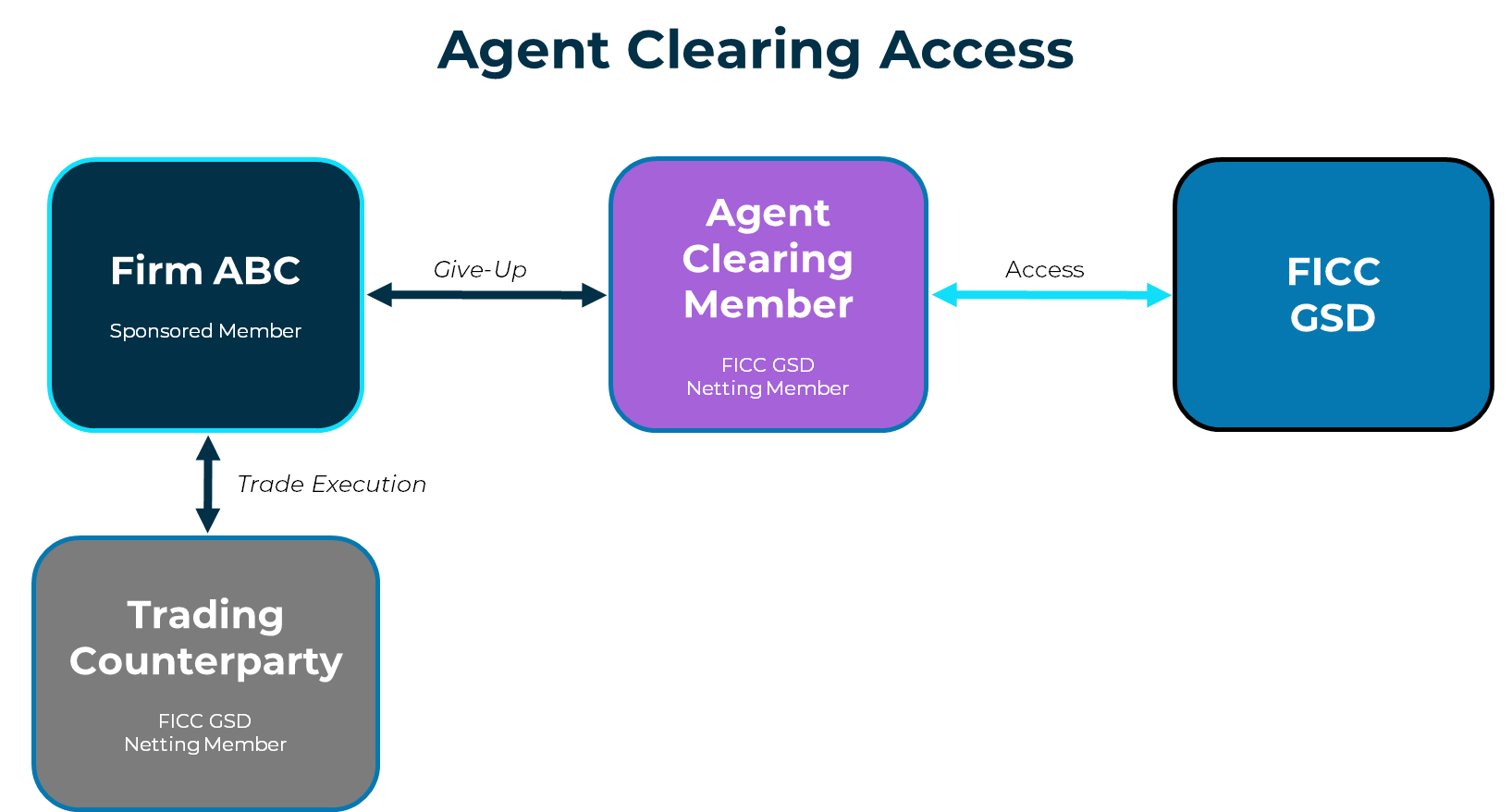

Since the completion of the UST Clearing regulation, a “new” access model has been introduced by FICC GSD, called the Agent Clearingmodel ('ACM'). The ACM has been introduced with primary target to support 'Done-Away' trading, however, 'Done-With' trading can also be supported.

The ACM model is expected to be prevalent for UST central clearing in the future. The main distinction between the Sponsored model and Agent Clearing model is that the Agent model is specifically designed to support central clearing for trades that are executed by any counterparty on the street. The Agent Clearing Member will take "give-up" trades from clients and submit for central clearing on their behalf.

However, the Agent Clearing model is not exactly new, as the model has been spun out of multiple other domains. Indeed an equivalent "Agent" model is commonly seen in derivatives markets today, for both cleared OTC derivatives and futures clearing through a CCP. As such, the Agent model is anticipated to be widely used within other CCAs who currently support derivatives clearing, once they come to market with their respective UST Clearing service offerings.

There is not a separate FICC GSD membership type for Agent Clearing Members, or ‘ACMs’ that focus on ‘Done-Away’ trading. ACMs are required to be full Netting Members and must be able to meet the full set of daily obligations for Client and House trades.

As it stands today with GAAP (generally accepted accounting principles), the Agent Clearing Model does not permit ‘Done-Away’ UST Repo to be recorded off balance sheet, differing from the treatment of Sponsored Repo. In turn this subjects firms to higher capital requirements for leverage ratios. If the current rules are not changed, the Agent Clearing model may not be economically viable for Netting Members to support ‘Done-Away’ central clearing. Notably the current accounting rules for UST Clearing differ from derivatives clearing, where the clearing counterparty can record client trades off balance sheet.

These details are still being worked out at the SEC, but there is an intention to offer a balance-sheet friendly way for service provider firms to support both ‘Done-With’ and ‘Done-Away’ activity.

Note: There is a high probability that select existing Sponsoring Members will provide both ‘Done-With’ and ‘Done-Away’ models to their end clients. We will know more once firms build out their Agent Clearing Model and publicly share their offerings.

The below table now includes the Agent Clearing Model , alongside the Executing Firm Customer, both of which have been introduced in line with the 'Done-Away' model.

See below for a summarized set of takeaways from our UST Clearing Kickstarter.

The UST market is in the midst of significanttransformation, driven by the SEC regulations to centrally clear UST Cash and Repo trades

Expect to see via new CCA entrants (e.g. CME, ICE, etc), the build-out of new UST services, new cost and margining models

We should also expect an evolution in the way firms seek liquidity and yield related to cash and UST securities

An increased UST Clearing cost base will also force firms to re-assess their end-to-end operating model, with many firms having a higher focus on analytics and optimization, across funding, operations and IT costs

In-scope firms should quickly mobilize their UST Clearing programs, if not done so already. Compliance dates will come quickly and front-to-back operating model transformation will be required at many firms.

Key early tasks include scope impact assessments, followed by early strategy decisions on access models and service providers as applicable

Whether you are a planning on increased centrally cleared volume, want to build new services, need to expand your UST Clearing access, or are brand new to UST Central Clearing, there is plenty of work ahead

Most buy-side firms and smaller market-making firms will leverage an indirect access model for mandatory UST Clearing, where they rely on service providers for access to the CCA(s)

This is due to high operational set-up and ongoing costs asscociate with the 'direct' access model, whcih requires full Netting Membership

In many cases, a Netting Membership may not be available to smaller firms, or is deemed impractical

Key indirect access models include:

Sponsored Member Model (‘Done-With') – Where one or more Sponsoring Members act as trading counterparty and access point for central clearing

Agent Clearing Model (‘Done-Away’) - Where an Agent can act as a single access point to the CCA across trading with multiple counterparties, via trade novations

The Sponsored Repo model is mature and has been in place for decades, with volumes of centrally cleared repo increasing considerably since COVID-19 and even since the SEC’s mandate was announced on December 13, 2023

Market experts believe that the Agent Clearing or ‘Done-Away’ model will be necessary to support the increased volumes of in-scope trades that require central clearing. Further market coordination is required to define whether the Agent model is financially viable, including whether trades can be treated 'off balance sheet', as per the derivatives model.

Look out for more expertise-led Tonic content on UST Clearing, and other hot industry topics.

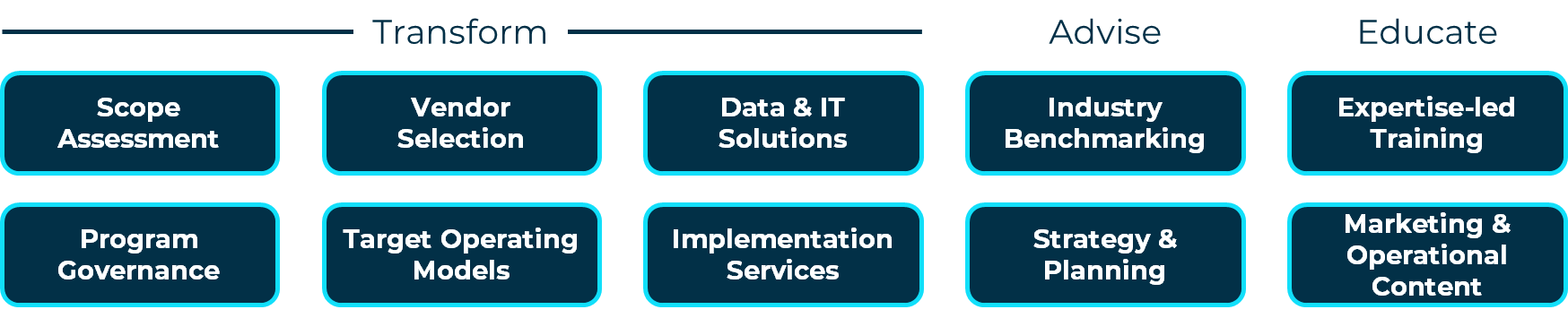

Tonic UST Clearing Services

Tonic provides an expertise-ledsuite of UST Clearing services, covering Transform, Advise and Educate modules.

All Tonic services are underpinned by our market practitioners, who come armed with the deep domain &transformation expertise required to accelerate our clients’ goals.

We have extensive experience as a regulatory transformation partner, with our practitioners successfully executing major, front-to-back programs such as Uncleared Margin (UMR), CSDR,US T+1 Settlement and More.

Our modular suite of Tonic UST Clearing services is shown below:

Critical business goals that we protect for our clients include:

Accelerated regulatory implementation

Optimal operating model definition, for resilience, scalability & growth

Long-term commercial success

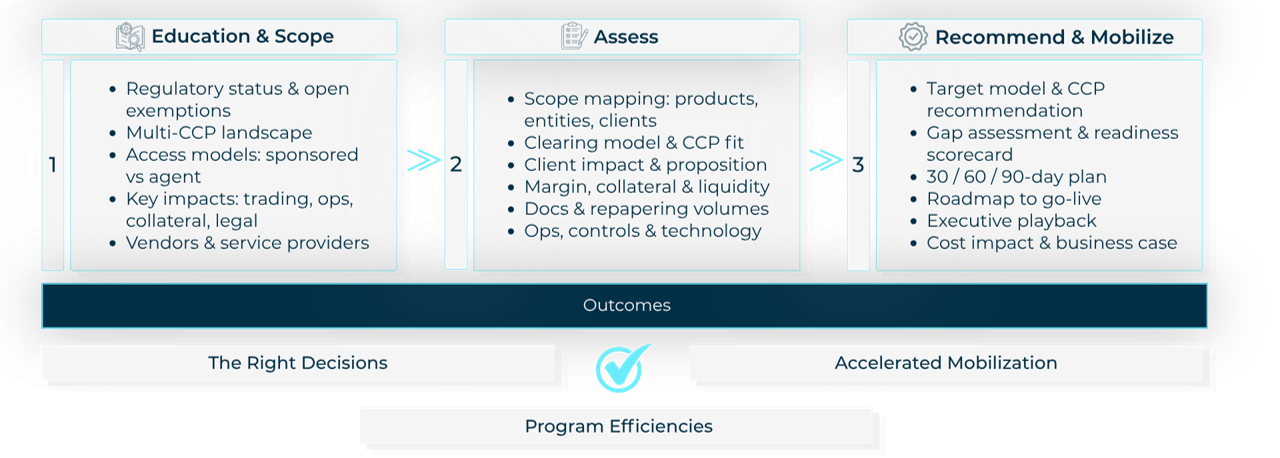

Tonic U.S. Treasury Clearing Health Check

For major transformational programs such as UST Clearing, our Tonic Health Check is a high-value tool to kickstart your firm’s compliance and the right solution decisions.

Tonic’s UST Clearing Health Check leverages our deep domain and transformation expertise to deliver ahigh-quality set of outputs to our clients, including:

High-quality UST Clearing education

Targeted scope impact assessment

Tailored recommendations, covering both market solutions and program approach

%20(10).png)

%20(9).png)