Part 2 of Tonic's detailed UST Clearing content is a deep dive on the UST Clearing access models, again with focus on the FICC GSD options, as it is currently the only Covered Clearing Agency available.

In the following, we will provide a summary of 4 access models with pros and cons, a workflow diagram, and closing comments. This info is most helpful to firms who are newer to clearing and need to decide how they will access central clearing, along with number of service providers to best fit their business needs.

We are focused on UST Repo transactions when discussing the access models and diagrams because the repo clearing is expected to be "net new" to many firms on the buy-side or who are not centrally clearing USTs today. Firms that are already netting members of FICC GSD likely already have models in place, and can clear both UST Cash and Repo trades today.

Reminder of UST Clearing Compliance Dates:

For UST Cash Trades - Compliance date is December 31, 2025.

For UST Repo Trades - Compliance date is June 30, 2026.

We will now go down another level and share the high-level workflows for the different UST Clearing access models, with continued focus on FICC GSD as the UST CCP.

Below are the four key access models that we will cover. We are tying 'Done-With' and 'Done-Away' clearing support with specific models today, because Sponsored Service has historically only supported 'Done-With' trading, and Agent Clearing was specifically introduced to support 'Done-Away' trading. In the future, we expect Sponsoring Members and Agent Clearing members to support both 'Done-With' and 'Done-Away' trading through central services.

Direct Access (Netting Membership)

Single Sponsoring Member (‘Done-With’)

Multiple Sponsoring Members (‘Done-With’)

Agent Clearing (‘Done-Away’)

Please Note: In the Direct Access model diagram, where both trading parties are Netting Members, both legs of the repo are novated to FICC and centrally cleared. In the subsequent diagrams, we provide the trade and settlement flows for the end-leg of a same-day settled repo. On same-day settled repo with service provider access, the open-leg is settled bilaterally and only the end-leg is novated, matched and then settled with the CCP. UST Repos where the start-leg is settled T+1 would have both start and end legs centrally cleared.

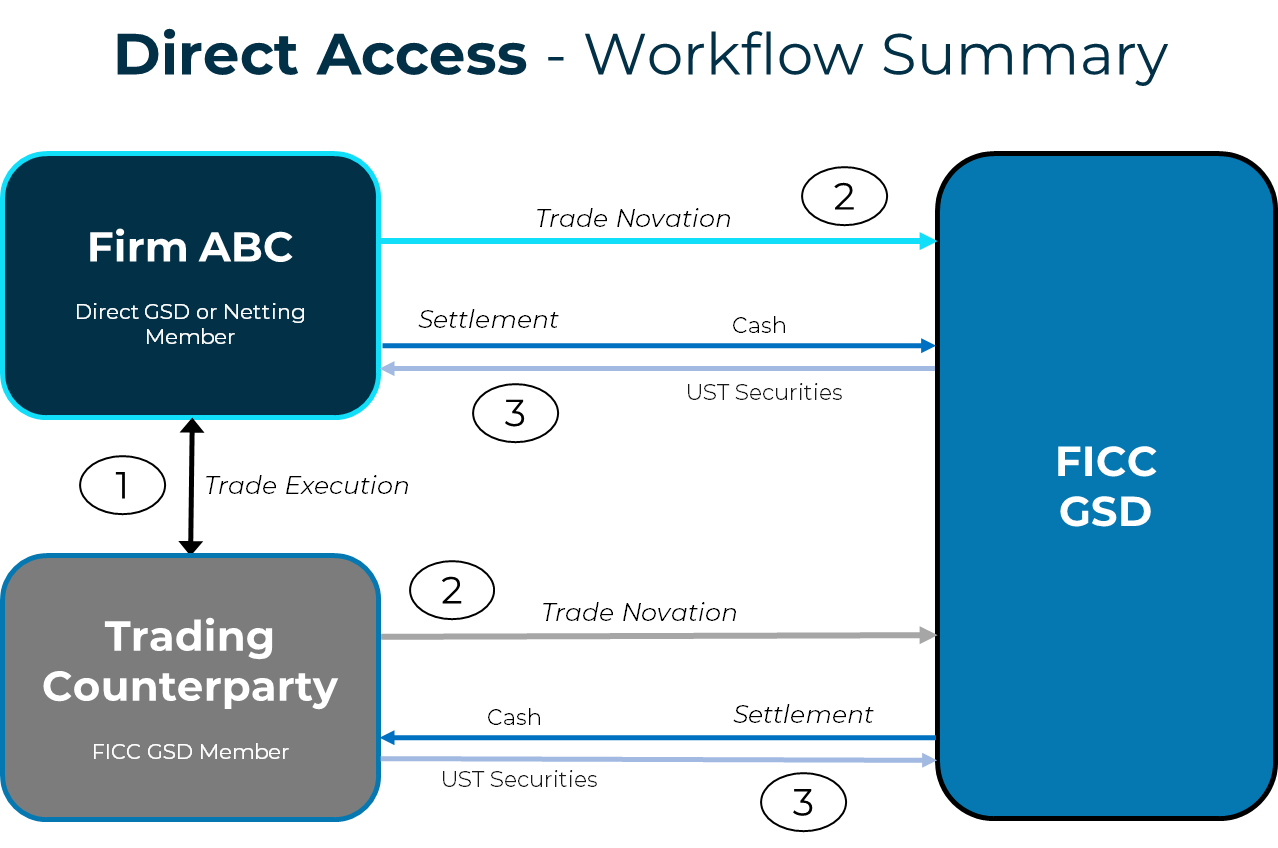

(1) Direct Access Model

There will be a subset of firms that set up directly with FICC GSD to become a Netting Member, under the direct access model.

A quick summary of what is required of a direct Netting Member is below, along with the high-level pros and cons of the direct model:

Firm meets the Qualifying Criteria for full Netting Membership

Firm covers the Clearing Fund (CCLF) and Twice-Daily Margin Obligations (based on FICC VaR Margin Model) directly with FICC GSD

Firm manages their own Trade and Settlement workflows directly with FICC GSD

Key Workflow Steps:

Firm ABC executes trade with a Counterparty, both are FICC GSD Netting Members

Firm ABC and Counterparty both novate the end-leg of the trade to FICC GSD as CCP

Firm ABC and Counterparty settle the end-leg directly with FICC GSD, as opposed to bilateral settlement between the trading parties

Closing Comments:

Any firm looking for a new direct access model and netting membership to FICC GSD should be well-equipped to handle the high costs and heavy operational build required. There should be a critical mass of cleared Cash and/or Repo UST trading to justify the financial and operational lift involved.

(2) Single Sponsoring Member (‘Done-With’ supported today)

Sponsored repo has been around for nearly two decades, and a having a Single Sponsor Model would be the only access to non-mandatory central clearing. In the modern era and since 2017, post-FICC's broadening of the sponsored model, the trend has been to create multiple sponsoring member relationships across all types of businesses and firms. Especially with cash borrowers, who can be constrained by credit limits and dealer capacity, so it behooves organizations to have several sponsored relationships for repo clearing. We will cover the single sponsor model below, as the most simple way to access central clearing, and also highlight the pros and cons

To set up a Sponsoring Member relationship, the Sponsoring and Sponsored Members must establish a relationship via FICC GSD documentation. For the Sponsored Members, this is a far reduced lift vs direct membership and the only practical option to access UST central clearing.

As it is today, the Sponsored Member will trade directly with their Sponsoring Member ('Done-With'), and the Sponsoring Member handles all operational workflows and financial obligations to FICC GSD. The Sponsored Member will only trade and settle directly with their Sponsoring Member in this scenario. In this access model, the Sponsoring Member is able to take in a deal-spread on the repo trade for clients, which enables them to fund the clearing costs and margin obligations to FICC GSD. It's to be determined how service providing firms will cover costs of clearing and margin with 'Done-Away' in the Sponsored Model.

Key Workflow Steps:

Firm ABC (Sponsored Member) executes a trade directly with their Sponsoring Member

The Sponsoring Member novates both sides of the end-leg to FICC GSD

The Sponsoring Member settles the end-leg of the trade with FICC GSD

The Sponsoring Member then settles the end-leg of the trade with Firm ABC

Closing Notes:

The single Sponsor model was initially the standard, but firms are electing to have multiple sponsors, since 2017 and even more as the regulation became official. The increased volume since model inception in 2005 has gained popularity from 2019 through December 2023, when the SEC announced the adoption of the UST Clearing mandate. In September 2023, we saw about 800 billion in Sponsored Repo cleared through FICC GSD daily. We are now seeing close to 1.5 trillion in Sponsored Repo centrally cleared daily in September 2024, with a strong upward trend.

We focus on repo here, because most Sponsored Members will not be required to clear most UST cash trades, but they will be required to clear most UST repo trades post June 2026. UST Repo is a critical tool for many buy-side firms, whether requiring liquidity or seeking yield on cash in the market daily.

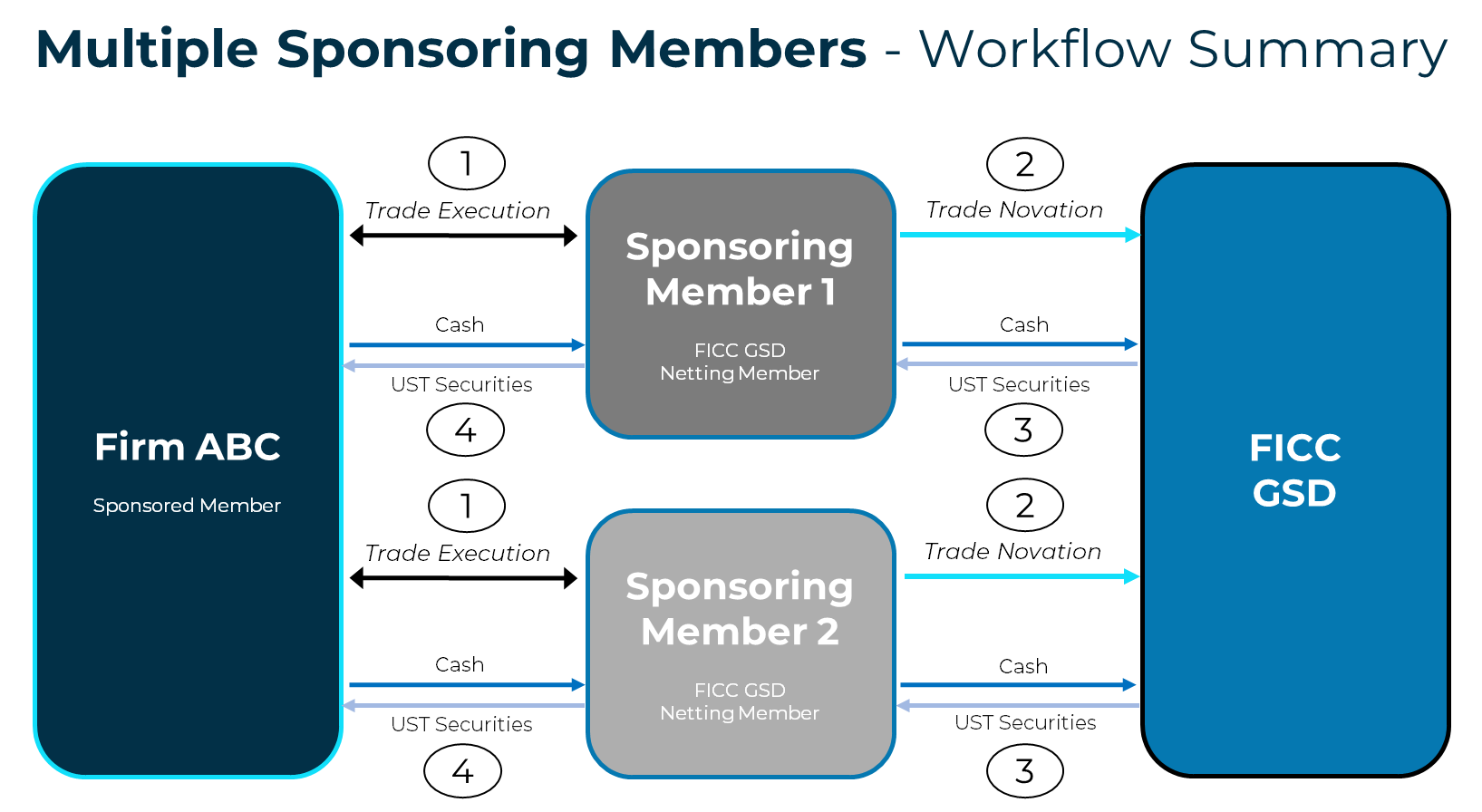

(3) Multiple Sponsoring Members ('Done-With’ supported today)

As mentioned prior, many buy-side firms have already shown appetite for multiple access points to FICC GSD, via signing up with a number of different Sponsoring Members.

As UST Repo clearing becomes mandatory, a multiple Sponsors will allow client to meet their liquidity or yield-seeking needs with competitive pricing, while mitigating sole-provider or access risk.

The multi-Sponsoring model still utilizes ‘Done-With’ trading today, where the service provider is making the market for the client and supports all central clearing workflows on the same trade. It is effectively the same model as the single Sponsoring Member model, but with multiple providers and trading partners in play for a given client. The economics work the same as the Single Sponsored Model, where the deal-spread is earned by the Sponsoring Member to recoup clearing and margin costs. Reminder that the Sponsored Service can also support 'Done-Away' activity, and some providers are expected to offer this in the near future.

Key Workflow Steps:

Firm ABC executes trades directly with multiple Sponsoring Members, with terms agreed on each individual trade

The respective Sponsoring Members independently novate both sides of the end-leg to FICC GSD

The Sponsoring Members independently settle the end-leg of the trades with FICC GSD

The Sponsoring Members then independently settle the end-leg of the trades with Firm ABC

Closing Notes:

We are seeing a large number of clients and firms sign up with multiple Sponsoring Members in preparation for UST mandatory clearing. There is data to support this, as the recently published FICC GSD survey from 2024 has reported the preference for Sponsored Service (‘Done-With’) for access to central clearing, albeit with growing interest in usage of the Agent Clearing Model. Please see further findings from the FICC GSD Survey in the link below

Since the ‘Done-Away’ or Agent model is not yet widely supported or used in practice, the Multiple Sponsoring Member is being utilized to best gain access to FICC GSD central clearing while maintaining diversity in trading partners and avoiding concentration risk.

(4) Agent Clearing (introduced to support 'Done-Away')

As mentioned before, the Agent Clearing model has been recently ‘re-introduced’ by FICC GSD, spun out of the correspondent and prime broker models. Similar to the Sponsoring Member model, the client or buy-side firm relies on the Agent for access to central clearing for trade and settlement workflows.

Differing from current Sponsored Services today, the Agent Clearing Model is focused on central clearing of trades executed by clients with external (non-clearing agent) counterparties, i.e. 'Done-Away.' This model can provide a broad set of trading counterparties with a single service provider for UST central clearing. Another difference from sponsored services, is that the end client, called ‘Executing Firm Customer’ is not required to be a member of FICC GSD and all liabilities to FICC GSD reside with the Agent Clearing Firm. Agent Clearing Members will likely support 'Done-With' trading that is executed by their repo desk as well, but FICC GSD has specifically introduced the Agent Clearing Service to support 'Done-Away.'

The economics between 'Done-With' and 'Done-Away' are different, as the deal-spread is not directly earned by the service provider on the 'Done-Away' trade. The deal is made externally and then given up to the service provider. It should be expected to see some pass-through costs on the 'Done-Away' trades and service models that involve margin collection from the clients to support daily obligations.

The Pros and Cons are particularly important for this access model. It’s attractive in theory, but it’s not widely used in the market today and the offering from ACMs (Netting Members) is not developed. We are not yet sure how this will play out with service providers or the additional CCAs expected to support the ‘Done-Away’ model.

Key Workflow Steps:

Firm ABC executes trade with a Trading Counterparty

Firm ABC and Trading Counterparty settle open leg bilaterally

Firm ABC then gives-up the same trade to the Agent Clearing Member (ACM)

Counterparty and ACM both novate the end-leg to FICC GSD

Counterparty and ACM settle the trade with FICC GSD

The ACM settles the end-leg with Firm ABC

Closing Notes:

The Agent Clearing model is not a tangible offering for clearing US treasury repo today - it's expected to largely support 'Done-Away' trading, but can support 'Done-With' as well. The recent FICC GSD White-Paper highlights the increased interest in ‘Done-Away’ central clearing support, but we are yet to see the market provide solutions and options to support the “give-ups” on repo ‘Done-Away’ with other counterparties.

As addressed in Part 1, the ACM service would closely resemble the FCM and Cleared Counterparty models that we currently see in the futures and cleared OTC markets, where parties will centrally clear any trade executed in the market on the client’s behalf, regardless of the initiating counterparty. We are yet to see what type of cost and margin models setup by Agent Clearing Firms will be, but it’s likely to see more pass-through on clearing costs and margin collection, as the deal-spread revenue in the 'Done-With,' Sponsored Model is not present in the 'Done-Away,' Agent Clearing Model.

The market is anxious for more info and service offerings in this space, which can help solve their needs for liquidity/yield across multiple trading partners, while simplifying the access and operational workflows for central clearing.

Stay tuned for updates on the Agency Clearing Model and other updates related to access models on the Tonic UST Clearing Webpage

See below for a summarized set of takeaways from the detailed Access Models

There are 4 keys access models that are expected with UST central clearing through FICC GSD as firms seek compliance. 'Done-With' and 'Done-Away' can be supported by all service provider models, however there is expected to be linked concentration as listed below.

Direct Access (Netting Membership)

Single Sponsoring Member (‘Done-With’)

Multiple Sponsoring Members (‘Done-With’)

Agent Clearing (‘Done-Away’)

There may be a select number of firms that elect to gain direct access to FICC GSD and run the central clearing operational connectivity in-house

These firms will need to qualify to be a FICC GSD netting member and be ready to support the full lifecycle and costs of central clearing

Practicality should be a key focus when looking to setup as a netting member. There should be a critical mass of UST Cash and/or Repo trades with a strong business case to setup as a full netting member

Most buy-side firms and other firms that less active in the UST repo space should expect to find one or many serviceproviders for access to central clearing. It's likely that most clients will seek multiple service providers for access to central clearing, because there are client based credit limits and capacity constraints at the service provider for repo. UST Repo availability is critical for many firms, so ensuring sufficient access to mandatory central clearing post June 30, 2026 is necessary.

The FICC GSD white paper has informed that there is strong appetite for the Sponsored Service model, with growing interest in the Agent Clearing Model. The Sponsored model has been around for decades and is a mature access model, while Agency Clearing is "new" and notyetavailable broadly in the market. Firms should be talking to service providers about services and timing of availability as the compliance date nears. June 30, 2026 will come quickly and firms that depend on UST repo need to have ample access.

Economics for Agent Clearing and 'Done-Away' are yet to be determined, so firms need to stay tuned if they are seeking this setup. The deal-spread is not earned by the service provider on 'Done-Away' trades, so clients should expect some additional cost and/or margin models to emerge with Agent Clearing services. There is also the complication with the accounting rules and balance sheet treatment at the service provider that was addressed in Part 1. It is expected that the SEC will help define a balance sheet friendly for 'Done-Away' repo clearing, so the market will need to stay tuned for the viability. The industry considers this change critical for the success of the UST clearing initiative.

The onboarding effort for firms to get access to central clearing, whether direct or indirect with service providers, is not a trivial exercise. Firms will need to paper regardless of their access model and service providers, and there will be queues that build up as the compliance dates near. Firms are advised to mobilize their UST Clearing programs immediately to best prepare for their UST clearing needs before it's too late.

Look out for more expertise-led Tonic content on UST Clearing, and other hot industry topics in the future

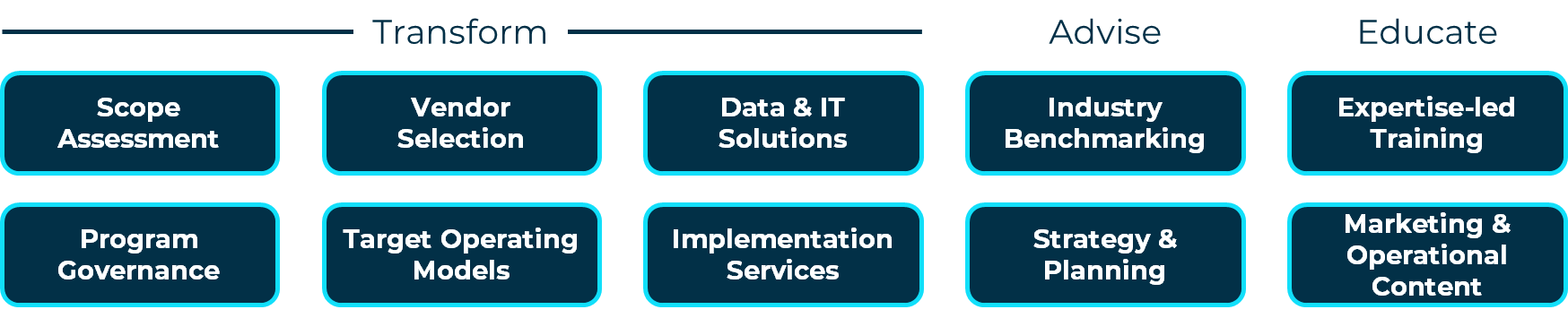

Tonic UST Clearing Services

Tonic provides an expertise-ledsuite of UST Clearing services, covering Transform, Advise and Educate modules.

All Tonic services are underpinned by our market practitioners, who come armed with the deep domain &transformation expertise required to accelerate our clients’ goals.

We have extensive experience as a regulatory transformation partner, with our practitioners successfully executing major, front-to-back programs such as Uncleared Margin (UMR), CSDR,US T+1 Settlement and More.

Our modular suite of Tonic UST Clearing services is shown below:

Critical business goals that we protect for our clients include:

Accelerated regulatory implementation

Optimal operating model definition, for resilience, scalability & growth

Long-term commercial success

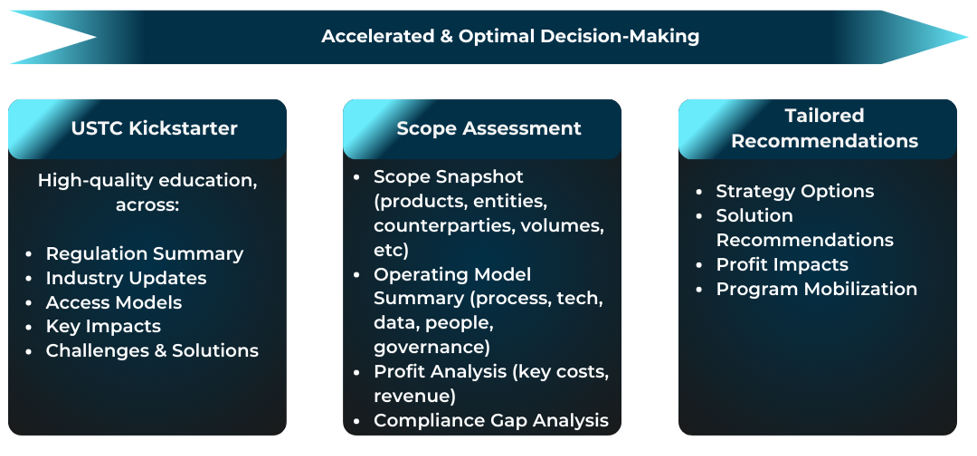

Tonic U.S. Treasury Clearing Health Check

For major transformational programs such as UST Clearing, our Tonic Health Check is a high-value tool to kickstart your firm’s compliance and the right solution decisions.

Tonic’s UST Clearing Health Check leverages our deep domain and transformation expertise to deliver ahigh-quality set of outputs to our clients, including:

High-quality UST Clearing education

Targeted scope impact assessment

Tailored recommendations, covering both market solutions and program approach